Table of Contents

It is incredibly valuable to learn when it's the right time to stop trying to pay off debt yourself. The do-it-yourself path, where you build a budget and follow a common payoff strategy, like the debt snowball or avalanche, is the right instinct for most people. But for some people it is a strategy that cannot mathematically work, and spending years trying to make it work costs far more than getting help would have.

In this article, we explore the honest truth about paying off debt yourself. We won't tell you to give up after the first hard month, but we will illustrate the difference between a payoff plan that is merely difficult and one that will truly not work, so you can stop wasting time and money on the latter.

Why DIY payoff comes first

For most people burdened by debt, getting yourself out of it seems like the best option, and it should definitely be the first thing you try. DIY debt payoff strategies cost nothing, do nothing to your credit, and keep you in control. If you haven't tried building a budget and committing to a payoff strategy, that is the best place to start. Check out our guide on the debt snowball method which walks through the most beginner-friendly approach, and if you want to weigh it against the popular avalanche method which pays by interest rate, we compare them in snowball vs. avalanche.

Most debt isn't a matter of a math impossibility, it is a cash flow and behaviour problem. This is why self-directed payoff can be a great option for so many people. If you can free up a few hundred dollars in your budget each month to go toward paying down your debt beyond just the minimums, then payoff strategies like the debt snowball do the rest. The question this article focuses on is what to do when that is not your situation, when you have crunched all the numbers and the plan still doesn't work.

The one math test that settles it

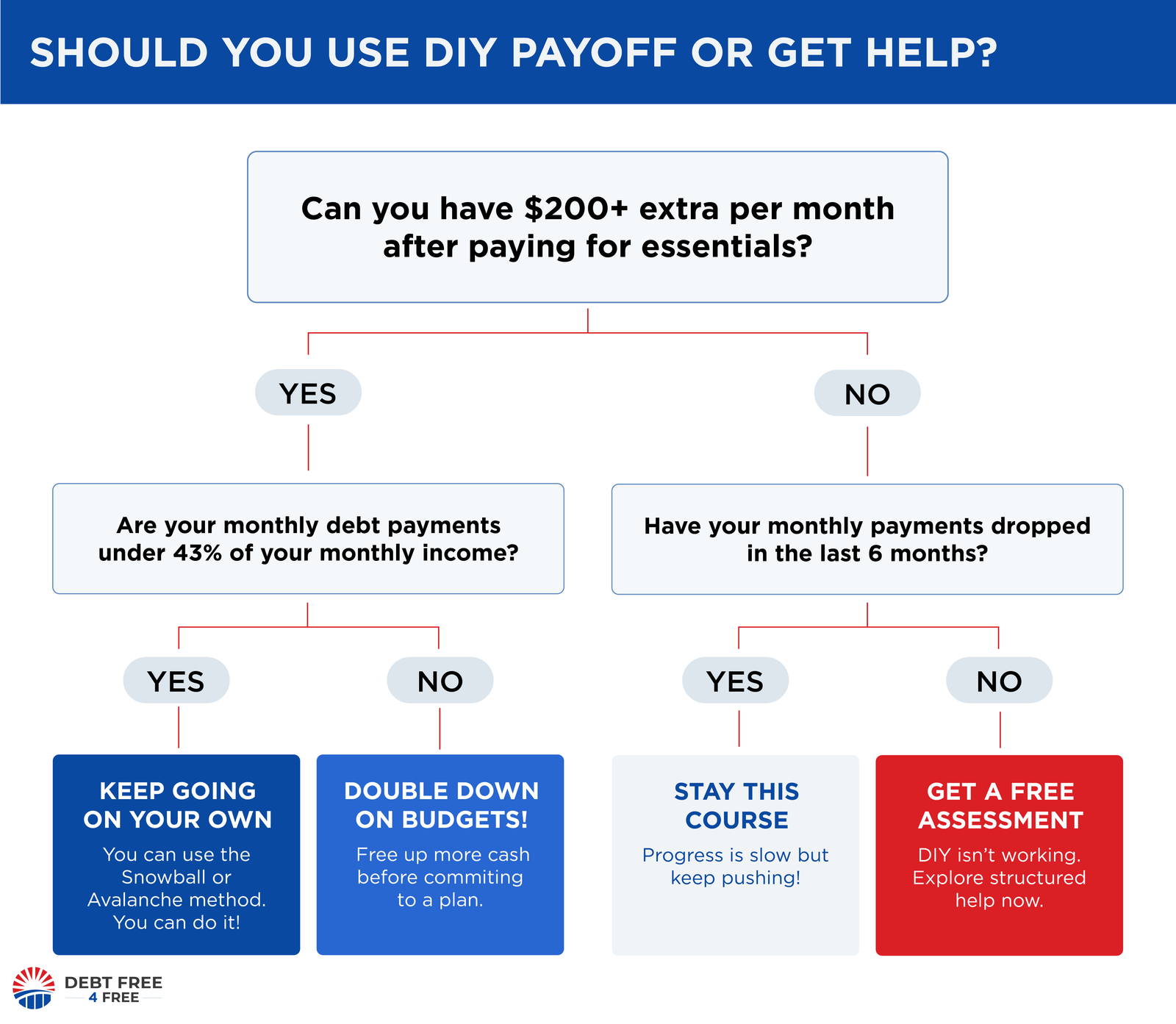

When making these critical decisions about your debt, it is best to start with the math because it is the most objective signal. Begin by adding up the minimum payments on all your debts. Then compare that total amount to your take-home income. No payoff strategy can make up for you not having the extra money to pay down your debts. All of the most popular debt payoff methods rely on that extra money that can be put toward accelerating your payoff timeline.

There is a related figure, called debt-to-income ratio, or DTI, which lenders often use. It refers to your total monthly debt payments divided by your gross monthly income. This figure is a useful benchmark in determining how you should approach becoming debt free.

| Debt-to-income ratio | What it usually means |

|---|---|

| 36% or below | Generally manageable. Self-directed payoff should work. |

| 37% to 42% | Tight but workable with an aggressive budget. |

| 43% to 49% | Approaching unmanageable. Worth exploring outside options. |

| 50% or above | A strong signal that you may be carrying more debt than your income can realistically support. |

These thresholds are shaped by how lenders and credit experts view DTI, with a ratio under 36 percent being considered generally healthy and anything above 43 percent being viewed as a red flag. They are guidelines, not law, but if your DTI is well above 43 percent, paying off your debt by yourself is going to be much more challenging.

Can a realistic extra payment actually shrink your balances within a few years? If yes, keep going on your own. If your minimums alone already eat most of your paycheck, the order of payoff is not the problem, and no method will fix it.

7 signs it is time to get help

Establishing your DTI range is a great foundation but you need more to determine your best next step. Below we explore seven common signs that your DIY payoff has run its course and it is time to get real help. If you only have one or two of these markers, don't panic. But if these start stacking up to describe your situation, it may be time to move beyond the self-directed path.

- You can only afford the minimum payments. If your minimum payments already consume all of your left-over income, your balances will barely budge, because most of those payments are going to interest. This is the single strongest and most common sign that DIY debt payoff will not work for you.

- You are using one card to pay another. If you are needing to take out a cash advance or open a new card just to cover a payment on a different card, you should treat it as a clear sign that your cash flow is not sustainable.

- Your balances are flat or rising despite paying every month. If you have been making your minimum payments each month for years and the total balances are still stagnant or increasing, you may need to look for a different solution.

- You have no emergency savings at all. If paying the minimums leaves you with nothing left to set aside, the next unexpected expense, or an unforeseen emergency, will set you back and you will lose the ground you've gained.

- You are missing payments or getting collection calls. Late payments and collection calls aren't just stressful, they damage your credit and are a signal your current strategy is not working.

- The realistic payoff timeline is more than five to seven years. If an accurate, honest calculation shows it will take almost a decade to pay off your debts, the plan may be unsustainable and you should reassess.

- The stress is affecting your health, sleep, or relationships. Debt harming your wellbeing is a cost that truly counts. If the stress is too much to bear, it may be time to look for other options.

A plan that is merely hard is worth pushing through. A plan that cannot mathematically succeed is worth replacing. The skill is telling them apart honestly.

Not sure which side of the line you are on?

The free Credzy plan helps you see your real numbers, your true payoff timeline, your DTI, and a shortlist of options matched to your situation, with no fees and no credit check. Start your free Credzy plan and get a clear picture in a few minutes.

See My Free Plan →Getting help is not failure

It is easy to fall into the trap of thinking that asking for help with your debt means you did something wrong, or you just didn't try hard enough. This paradigm keeps people stuck for years. The goal isn't to win a contest of willpower, it is to become debt free. If a different path gets you there faster and with less damage, it is the responsible choice, not a failure.

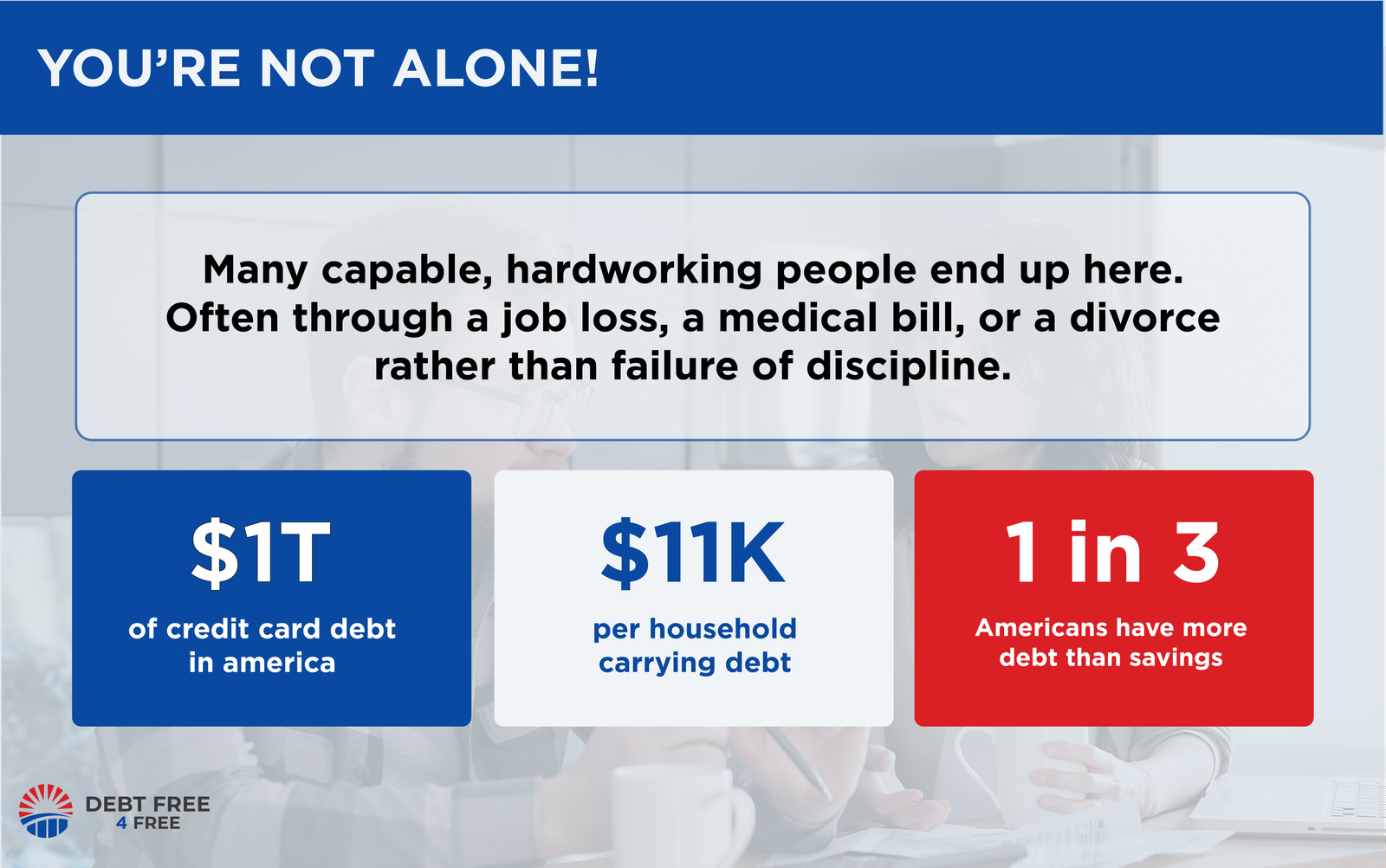

It is also good to remind yourself that you are not alone. You are facing a common problem. Americans carry well over a trillion dollars in credit card debt. There are millions of hardworking, capable people that end up in a situation just like yours. Whether it was a job loss, a medical bill, a divorce, or just getting carried away with credit cards, getting into debt is nothing to be ashamed of and needing a structured solution that works for you puts you in common company.

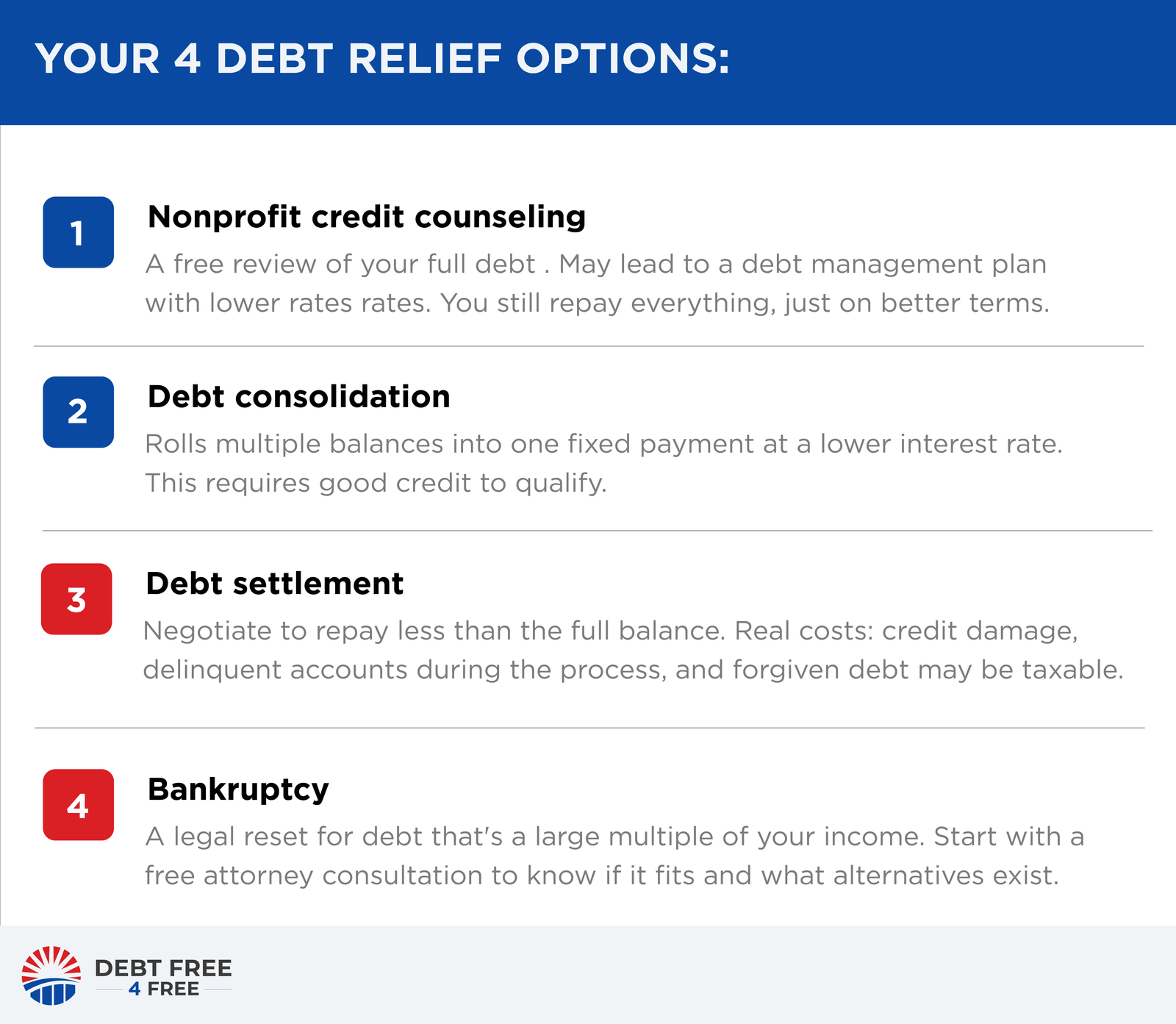

What real help actually looks like

Help doesn't always mean an expensive program and there is not one catch-all solution that will work for everyone. The options massively vary and range from free to paid, and from low impact on your credit to high. In this section, we will review some of the key options at your disposal.

The debt relief space has plenty of high-pressure sales operations. Keep your guard up and be on the lookout for scams and promises that look too good to be true.

Where to go from here

If several of the signs above sound familiar, you do not have to commit to a program to start getting clarity. The most useful first step is simply to see your real numbers laid out, your true payoff timeline at your current payment, your debt-to-income ratio, and which options actually fit your situation, before anyone asks you to sign anything.

That is exactly what a free assessment is for. You can run your numbers, see honestly whether self-directed payoff still has a realistic path, and review a shortlist of matched options if it does not, all with no fees, no credit check, and no obligation to move forward. The point is to replace the uncertainty with a clear picture so you can make a decision instead of just worrying about one.

The bottom line

Paying off debt on your own is the right place to start for most people, for a lot of them it is also where they will reach the finish line. But self-directed payoff is not the right path for everyone or every situation, and it will only get you further behind if you keep grinding on a method that doesn't work for you. If you are able to set aside an extra payment that can actually shrink your balances over the next few years, keep working at it yourself. However, if your minimums already take up most of your income, and you can't find much extra money to fuel the common payoff strategies, you need to recognize when it is time to reassess.

Again, this is not giving up. It is making the choice to take a path that can actually help you become debt free. Whether you get into consolidation, build a tighter budget, go into settlement, the best thing you can do is take an honest look at your situation and the numbers before making your decision.