Table of Contents

When people compare the debt snowball and debt avalanche, they are usually looking for reassurance that one method is superior and the one they should choose. But it's more nuanced than that. So, here is the truth right up front: the avalanche saves you more money, but the snowball keeps more people motivated enough to pay off their debt entirely. The gap between the two is much smaller in reality than the internet and popular finance figures would have you believe. The right choice depends less on the math and more on which plan you will actually stick with.

Both methods actually agree on the essential flow. You pay the minimum on every debt so that nothing goes late and your credit isn't destroyed, and you take whatever extra money you can find and throw it towards paying down one debt at a time. The only difference is which debt you should prioritize paying down. This guide will walk through this decision and exactly what it costs you either way.

The one difference between them

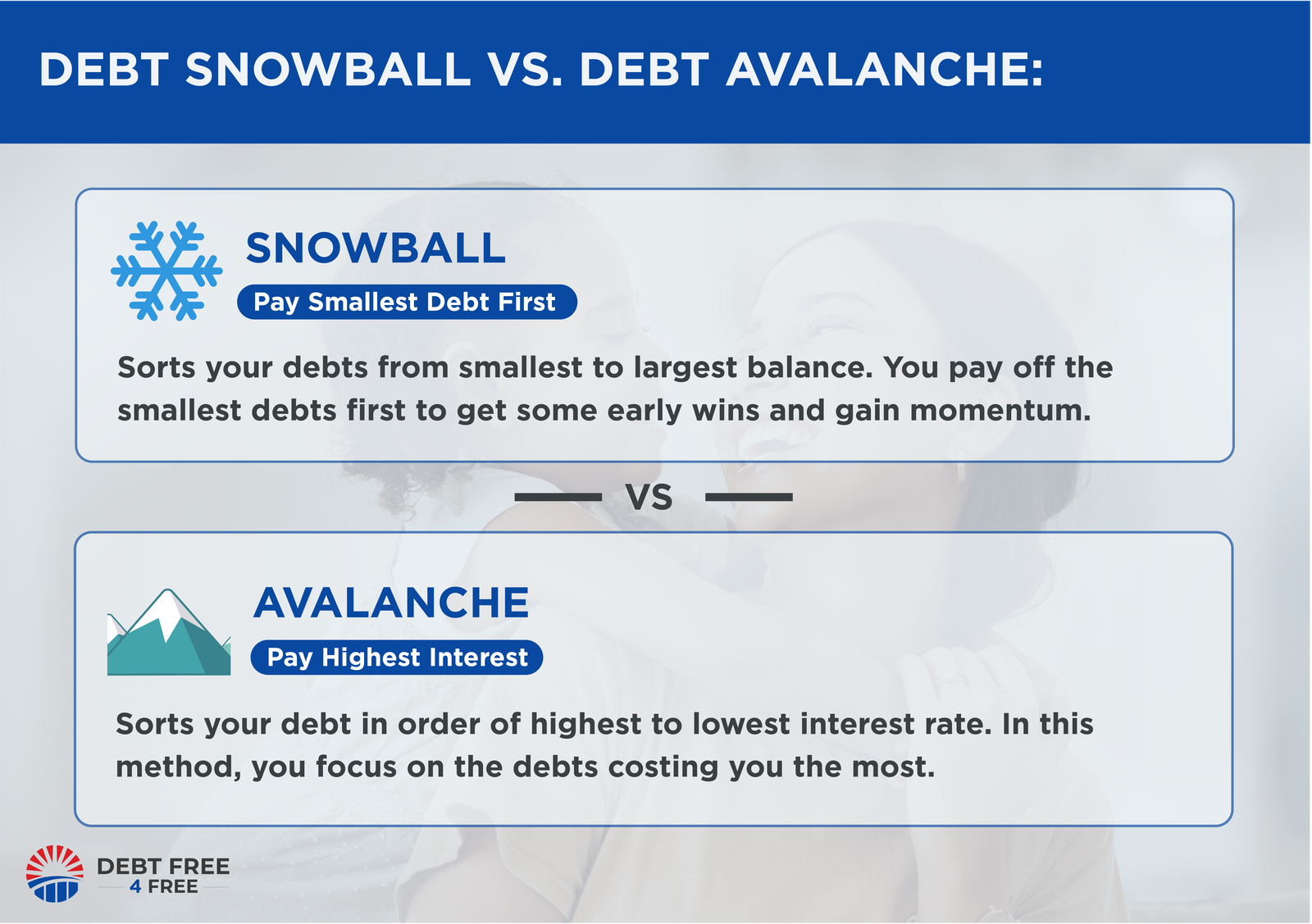

When you strip away the marketing buzzwords, these two methods are very similar with each of them being "debt stacking" methods. This means that you concentrate all of your pay-off efforts on one debt at a time while only maintaining minimum payments on the rest. The only thing that changes with each strategy is how you decide which debt to focus on.

This small ordering change is the entire difference between the two methods. If you want to learn more about the full mechanics of the smallest-balance-first approach, we cover the debt snowball method extensively in our complete guide to the debt snowball method.

How the avalanche works

If it were up to mathematicians, the avalanche would be the clear choice everytime. Interest is the cost of carrying debt, and your highest interest rate debt is the most expensive balance you owe. By getting rid of this debt first, you stop the interest from getting even more out of hand as soon as possible. This means that more of each future payment goes to principal pay-off instead of the lender.

With interest rates on buy-now-pay-later agreements, personal loans, and credit cards ever on the rise in 2025, paying off high interest accounts matters more than ever. According to leading sources like the Federal Reserve and data from LendingTree, the average credit card interest rate is roughly 21 percent. If one of your debts is costing you over 20 percent interest while another is at 6, the hack of the avalanche method becomes clear.

Highest interest rate first. It minimizes total interest paid and, by a smaller margin, usually shortens your payoff timeline.

How the snowball works

The snowball works by ordering your debts from smallest to largest balance rather rather than by interest rate. The math makes this seem irrational at first because you end up paying more interest than in the avalanche, but the snowball doesn't optimize for saving interest. Instead, it is optimized for momentum.

This momentum-first approach is backed up by decades of research. For example, one 2012 study by David Gal and Blakeley McShane at Northwestern University's Kellogg School of Management, published in the Journal of Marketing Research, found that the number of accounts a person closed predicted whether they would eliminate their debt, independent of how large those accounts were. Finishing a debt, the act of taking an account to zero, appears to be what keeps people going. The snowball is engineered to produce that finish as early as possible.

The avalanche is centered around the numbers while the snowball is more focused on human behavior.

This is why the snowball so often beats the avalanche in the real world even though it loses on paper. A method that costs slightly more but that you actually complete will always beat a cheaper method you can't sustain and end up abandoning after a few months.

Same debts, both methods

To see these strategies both in action, let's now run identical debts through the process prescribed by each method. In the scenario shown below, imagine you can put $700 per month toward paying off your debt and you owe the following.

| Debt | Balance | APR | Minimum |

|---|---|---|---|

| Medical bill | $1,200 | 0% | $40 |

| Credit card A | $3,500 | 27% | $90 |

| Car loan | $5,000 | 6% | $180 |

| Credit card B | $6,000 | 19% | $150 |

The two methods produce very different running orders.

| Order | Snowball (by balance) | Avalanche (by rate) |

|---|---|---|

| First | Medical bill ($1,200) | Credit card A (27%) |

| Second | Credit card A ($3,500) | Credit card B (19%) |

| Third | Car loan ($5,000) | Car loan (6%) |

| Fourth | Credit card B ($6,000) | Medical bill (0%) |

In the example above, we see the avalanche's advantage at its peak as it instantly focuses on the 27 percent interest rate card. However, in the snowball, you would clear the massive burden and stress of a major medical bill in only a couple of month and then go right to paying off the high interest card with renewed momentum.

When your smallest balance and your highest rate are the same debt, the snowball and the avalanche start in the same place and the choice barely matters. The methods only diverge meaningfully when your small debts are cheap and your big debts are expensive, like the example above.

How much does the avalanche really save?

Here is the part that gets exaggerated. In the example above, with roughly $15,700 in total debt and a $700 monthly payment, the avalanche would save somewhere in the range of a few hundred dollars in interest and finish perhaps a month or so sooner than the snowball. On a debt that takes a couple of years to clear, that is a real but modest edge.

The size of the avalanche's advantage depends on three things:

- The spread between your highest and lowest rates. A list where everything sits between 19 and 24 percent produces almost no difference. A list with a 0 percent bill and a 29 percent card produces a larger one.

- How long your payoff takes. The longer the timeline, the more interest is in play, so the more the order matters.

- How much extra you pay. The more aggressively you pay, the faster everything clears and the less the ordering can matter, because high-rate debt does not get the time to do as much damage.

For most households carrying a few thousand to the low tens of thousands in mixed debt, the realistic gap between the two methods is in the hundreds of dollars, not the thousands. That is worth knowing, because it reframes the decision. You are not choosing between a smart plan and a dumb one. You are choosing between saving a few hundred dollars and giving yourself an earlier psychological win. Both are legitimate priorities.

See both timelines side by side

The free Credzy plan lets you model your debts both ways, so you can see exactly how much interest the avalanche saves you and how much sooner the snowball hands you your first win. Start your free Credzy plan and compare in a couple of minutes.

See My Free Plan →Which one should you pick?

Use this as a quick decision guide. It is not about which method is objectively better. It is about which one fits you.

Choose the avalanche if…

- You are motivated by numbers and the idea of paying a single unnecessary dollar of interest genuinely bothers you.

- You have a clear rate spread, with at least one debt charging much more than the others.

- You have stuck to financial plans before and you trust yourself to keep going without frequent wins.

Choose the snowball if…

- You have started payoff plans before and lost momentum partway through.

- You have one or two small balances you could erase in the first month or two, which would feel great and prove to yourself the plan works.

- You know that staying motivated, not optimizing interest, is your real challenge.

If you read those two lists and the snowball describes you, do not let anyone shame you into the avalanche to save a few hundred dollars you will never see if you quit. The best method is the one you finish.

A hybrid that often wins

You do not have to be entirely limited to just one of these methods. Many people in your same position use a blend of these two methods, something that can often give you the benefit of both.

One common hybrid that may work for you is if you have a small balance that you can clear easily in the first month or two, pay this one down first for the quick win to start building momentum. This still gives you most of the savings of the avalanche. Another method is to use the avalanche as your default method but make exceptions for any debts that are uniquely stressful, paying those off as soon as possible to keep momentum and limit stress.

Regardless of whether you go with the avalanche or the snowball, the more important factor is the size of your extra payment, not the order of the payments. Freeing up extra funds to fuel your debt payoff will gain you more ground than any difference between these methods.

When neither method is the answer

There are some situations where both methods will fail for your particular situation. The snowball and avalanche each work only if you can set aside an extra payment on top of your minimums. If your minimum payments by themselves are already eating up most of your income, then these methods will not work.

If this sounds like your situation, the most useful step you can take is an honest assessment of your options rather than attempting a method where the numbers don't work out. Check out our guide on when to stop trying to pay off debt yourself to learn more about what options you have and to help you determine when it is time to put the self-directed route to rest.

The bottom line

The question of whether to go with the debt snowball or the avalanche isn't a matter of one being superior in every way. While the avalanche saves you more money through its focus on interest, the snowball gets you wins as early as possible to build momentum and completely cross debts off. For most of us, the difference isn't going to be thousands of dollars, so don't solely choose based on the math.

So the choice really comes down to you, your goals, and what it takes for you to stick with a plan. If you have had a previous plan stall out, the snowball may give you what you need to make sure that it doesn't happen again. Maybe saving the extra interest on the avalanche pushes it over the edge, or you could even go with some hybrid of the two and fiit a solution to your specific needs. The most important piece is simply that you make the effort to budget well and get your extra payment, make your payments on time, and stick with your plan.